Turbulent markets and rising interest rates – Why invest or stay invested?

In the current worldwide, economic turmoil it is only natural to ask whether it is worth investing or staying invested, especially when bank and building society deposits are rising. At least in the short term.

Given this, I think the following article, written by Ben Kumar, Senior Investment Strategist at 7 Investment Management (one of our investment partners), makes interesting and inciteful reading.

Investing through a recession

Ben Kumar

Senior Investment Strategist

If you’ve read the financial headlines recently, you’re probably a little nervous about a recession. And as Ahmer noted earlier, we share some of those concerns. At some point, a recession will happen – it’s part of the way the world works. And making sensible investment decisions during that recession is essential. That’s quite literally our job.

But it’s important to be clear on what we believe that job entails. Because when recession hits, it can be easy to think that the sensible investment decision is to be nowhere near the market. To move to cash. To avoid losing any money.

That’s not the case.

Our job is to make sure that the majority of our clients’ money is working over the long-term – we are not Dis-Investment Managers. To understand that, it’s helpful to understand our mindset, and what “success” means for our clients.

When “winning” matters …

In competitive sports, winning is everything. Your number of wins dictates your level of success. If you’re a football or rugby or cricket team, the ideal season would be one where you win every game and lose none.

Or look at a period in the career of recently retired Roger Federer. Between 2003 and 2008, Federer was unbeaten for 65 matches on grass, resulting in five successive Wimbledon titles. One loss, at any point, would have cost him one of those titles.

Whether it’s beach volleyball or boxing, chess or croquet, the optimal strategy is identical for every competitor. Maximise wins. Beat everyone else. If you win the most, you’ll be the most successful.

… and when it doesn’t

People talk about investing in the wrong way. There are “good” investments and “failing” investments. We hear about superstar stock pickers, league tables of their funds, and quarterly or weekly (or daily) “results”. Pundits appear on financial shows and in newspapers, talking excitedly about possible “winning strategies”. TV shows like “Billions” push the competitive narrative even further. Investing ends up being portrayed as a tournament.

Which it isn’t.

Investing isn’t a head-to-head competition. And if people get suckered into thinking about it competitively, they end up approaching investing in completely the wrong way – thinking about short-term results, instead of long-term outcomes. They get twitchy, and start equating portfolio declines with “losing”, and “losing” with “failing”.

But there’s no match or race to win when it comes to investing. No grand prix, no world cup, no Olympic final, no trophy. More importantly, no one-off event to “lose”.

Instead, the right mindset for investing is to approach it as you approach having a healthy lifestyle; as a long-term way of behaving which acknowledges that there’s no finish line or final whistle. You don’t “win” or “lose” a diet or an exercise regime – you just try to do the right things over time. If occasionally you drink and eat a little too much, or skip a workout, it doesn’t mean you’ve lost. You don’t abandon everything, and then wait for next season.

It’s a process, rather than a match. Fluctuations in markets happen. They’re an integral part of the experience of investing. Treating them like losses to be avoided is the wrong approach.

If you broadly stick to your process, over time you’ll see the benefits – whether physical or financial.

The secret to successful investing? Don’t worry about “winning” or “losing”

Adopting this process-driven way of thinking is especially important during recessionary periods, when the temptation is to make extreme portfolio decisions to try and avoid any pain. But much like going on a crash-diet causes backsliding, or trying to get fit quickly causes injuries, this is often counter-productive.

Investors who are trying to time the market over the course of an investment cycle often suffer whiplash. It won’t be until a recession is underway before they feel like they’re losing the match. They move to cash to try and avoid “losing”. Then the market bounces, but they buy back in too late to give themselves a change to “win”.

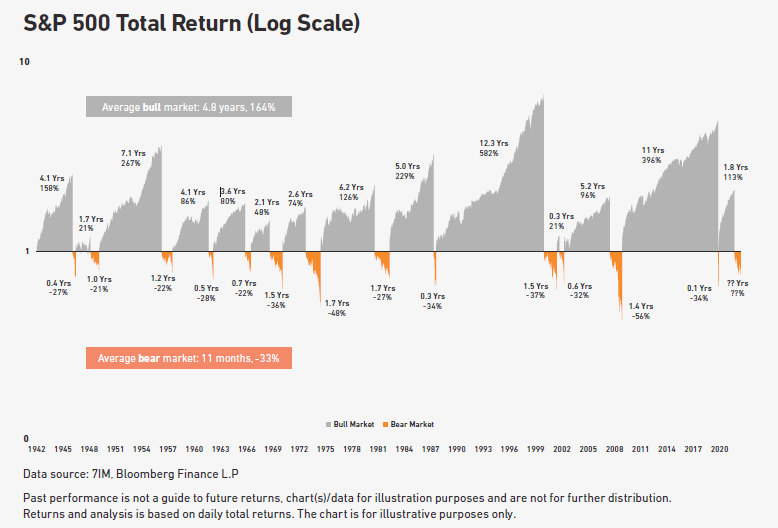

Looking at financial history helps us understand why timing the market – abandoning the process – is rarely a good idea. Click the chart which shows bull and bear markets going back to the Second World War (using US equity markets where there’s lots of data).

Figure 1: Bull and Bear markets in S&P 500. Bear market defined as 20% fall from previous peak. Bull market defined as gain from previous low of bear market.

Although the world has changed a lot in the last 80 years, the investment cycle has maintained a familiar shape. The heartbeat of market forces looks pretty similar through the decades. Neither good times nor bad times last forever.

The good times tend to be better than the bad. Bear markets see average declines of 33%. Bull markets see average gains of 164%. And the good times tend to be longer than the bad. Bear markets last an average of 11 months, while bull markets last an average of nearly five years.

But there’s another important statistic hidden away in the data – which explains the whiplash mentioned earlier. On average, half [1] of the total bull market returns occur in the first year following a bear market. That bounce back from recessionary lows to starting a new cycle happens violently and quickly – we saw that most recently during COVID-19.

Missing out on that first period of gains is catastrophic for returns.

So, our process is designed to avoid that mistake. We want to make sure we’re invested for the ups, which means accepting that we’ll be invested for the downs.

Of course, there are things you can do to soften the blow of those downs. We can reduce equities a little and have had some success over the last few years doing this. But this is a full-time decision not to be taken lightly – something we strongly advise our clients against trying. And even though we have had success, when we do reduce equities, we make sure that our clients still have enough equities for their long-term goals.

Other things you can do involve holding diversifying positions. Traditionally this would be bonds, that tend to make money (not this year!) when equities don’t. The trick here is to find diversifying assets that help you in the bad times, but don’t offset equities in the good times. Easier said than done. Our custom alternatives basket has played that role in the last few years.

The upshot is that we’ll try and mitigate the impact of the down periods on our clients’ portfolios, but we’ll never avoid them entirely. Doing that all but guarantees a lower return in the longer term.

[1] Actually 51.5%, but “half” is close enough!

What next?

As always, the Financial Planning Team are on hand to discuss any thoughts or concerns that you may have about investing, so please do not hesitate to contact us. In the first instance, please contact Chris Clayton.

Production

Production